Enter Your Email to Download the Guide and get 7 days of Tax Strategies Delivered to Your Inbox

How to Tap Into Suspended Passive Losses

Understanding how to tap into your suspended passive losses is important for all landlords and buy and hold real estate investors to understand. At some point, you'll likely be faced with the dreaded suspended passive loss. Your income will be too high and your real estate will be spitting out taxable losses thanks to all of the other awesome strategies you are using. If you are unaware as to how you can tap into suspended passive losses, then you'll leave a ton of money on the table.

We helped a client that came to us with $500,000 in suspended passive losses. $500,000! That means this real estate investor could have earned $500,000 of passive income without paying a dime in tax. Don't let your suspended passive losses get that high unless you are doing it on purpose to create flexibility.

Here are a few quick-hitting ideas to tap into your suspended passive losses:

- Acquire property that provides for better cash flow

- Sell property that has appreciated in value

- Qualify as a real estate professional (though this only stops future suspended passive losses from accruing; qualifying as a real estate professional will not allow you to unlock prior suspended passive losses)

- Invest in Passive Income Generators (PIGs) such as income oriented real estate limited partnerships or oil and gas investments. PIGs are are business investments in which you do not materially participate that are generating passive income from the beginning of your investment.

Managing your suspended passive losses effectively will allow you to optimize your cash flow and tax position. Don't let your suspended passive losses build up too much without taking any action.

If you want to track your suspended passive losses, pull up your tax return and scroll to Form 8582.

Ready to take your tax strategy to the next level? Click the link below to schedule a free 30-minute consultation where we'll determine if we can help you save more money.

What You Need to Know About the Tax Cuts and Jobs Act of 2017

On 12/22/2017, President Donald Trump signed the much talked about Tax Cuts and Jobs Act into law.

This was a fast process for such a large bill. The Tax Reform Act of 1986 took two years to hash out differences and approve. Two years. Fast forward to 2017, in a short seven weeks the GOP has developed, amended, reconciled, and signed into law a $1.456 Trillion tax bill.

We’re here to talk about what’s in the bill and how if may affect you. This section is not meant to be all encompassing. Instead, we’re pointing out key changes that affect landlords and buy and hold real estate investors.

That’s crazy fast. Not to mention the final bill has over 1,000 pages of text. Regardless, we’re not here to talk about whether or not our elected officials have read the bill they approved.

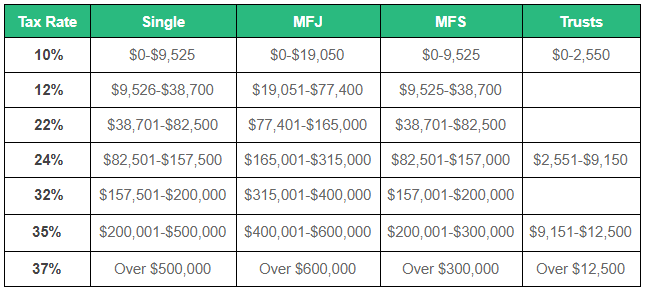

Tax brackets have been modified as you can see (2019 brackets pictured)

Itemized deductions changed, the most significant part was reducing the State and Local Tax deduction limit to $10,000

Our clients in high property and income tax states got hammered by the changes in itemized deductions, the State and Local Tax deduction being the main culprit. With the new changes, property tax and state income tax deductions were limited to an aggregate of $10,000. Many of our clients deducted 5x that amount in the past and this one change resulted in an increase of tax for many Americans. There remains confusion in the investor community as to whether the State and Local Tax deduction limitation also applies to rental property, however that is not the case as property taxes associated with a rental property will be considered a business expense.

Mortgage interest is deductible on the first $750,000 of new acquisition debt on primary and secondary residences. Originally, the proposed limits were much lower so it’s nice to see that they walked it back.

Home equity debt now poses a problem unless you use the proceeds to purchase or improve rental properties or for business. Interest on home equity debt is no longer deductible. Home equity debt includes refinances on your primary or secondary residences as well as HELOCs.

You will no longer be able to claim miscellaneous itemized deductions, such as tax preparation fees and unreimbursed employee expenses. Though you can still allocate tax preparation fees to Schedule C and E.

The Standard Deduction increased but personal exemptions were eliminated

The standard deduction has almost doubled. Single taxpayers will now claim $12,000 and married taxpayers will claim $24,000. This will cause fewer taxpayers to itemize deductions.

Personal exemptions have been eliminated. Taxpayers were previously allowed to take a personal exemption deduction of $4,050 per person they claimed on the tax return.

A boost for the Child Tax Credit

Though personal exemptions have been eliminated, the new rules surrounding the child tax credit will help balance things out. The Child Tax Credit amount increased from $1,000 to $2,000 per qualifying child. The refundable credit increased to $1,400. The income phase outs have increased to $200,000 if single and $400,000 if married filing joint.

Use of 529 Plans expanded

529 plans received a much needed boost. You can now use 529 plans to pay for private, public, and religious elementary and secondary schooling and qualified education expenses.

Alternative Minimum Tax (AMT) is still lurking, but affects less taxpayers

The exemption amounts have increased to $109,400 for married filing joint and $70,300 for all other taxpayers. The phaseout thresholds are increased to $1,000,000 for married taxpayers filing a joint return, and $500,000 for all other taxpayers (other than estates and trusts). These amounts are indexed for inflation. And unfortunately that means tax professionals still have to stumble through the AMT calculation each year.

Obamacare penalty eliminated

Good news for folks who are young, healthy, and don’t want or need health insurance. Beginning in 2019, you will not be assessed a penalty for not having health insurance. Unfortunately it’s bad news for everyone else who wants or needs health insurance. With the expected reduction in people buying health plans beginning in 2019, premiums are anticipated to increase.

20% Pass-Through Deduction added

This gets complicated fast, but try to hang in there. This “freebie” deduction is huge for landlords and business owners as long as your activity rises to the level of a trade or business. The deduction is granted after the calculation of AGI, so it’s a “below the line” deduction.

The deduction is available for sole proprietors, LLCs, and S-Corps generating qualified business income. If you are a partner in a business, you will receive the deduction based on your allocable ownership.

Service businesses will not receive a deduction at all, unless the taxpayers who own the service businesses have taxable income less than the below thresholds. The GOP brought down the hammer when they defined a service business as "any trade or business where the principal asset is the reputation or skill" except for engineers and architects though additional service businesses were later excluded.

If your total taxable income is less than $157,500 if single or $315,000 if married filing joint, then you just get a 20% deduction on combined qualified business income. You don’t have to worry about the additional calculations with wages and unadjusted basis.

The IRS released a safe harbor to help landlords qualify their rental properties for the 20% pass-through deduction.

C-Corporation tax rates reduced to a flat 21%

A 21% tax rate is a huge boon for C-Corporations. If you have previously considered C-Corporations in your tax planning, now is the time to revisit! C-Corporations can siphon off profits from other businesses and your portfolio. If used correctly, you can see a great reduction in your overall tax liability. Of course, there are major pitfalls to avoid as well, so don't try this on your own.

Bonus Depreciation increased to 100%

If you place assets with useful lives of less than 20 years into service beginning September 29, 2017, the asset will qualify for 100% expensing through bonus depreciation. Notably, rental properties have a 27.5 year useful life but if you perform cost segregation studies you will be able to use 100% bonus depreciation on the value allocated to the components with a useful life of less than 20 years.

It's not all fun and game. When you sell the assets, you will pay depreciation recapture tax, so while you get a nice write-off upfront, you’ll have to pay it back some day.

Lifetime Gift Exclusion doubled

Good news for folks with large estates. The lifetime gift exclusion has increased from $5MM to $10MM per person. This means you can pass $10MM of wealth tax-free.

Gifts are often a misunderstood concept. In any given year, you can gift anyone $14,000 each without incurring any tax filing requirements. So ff you’re feeling generous, you can gift me $14,000, and each person on my team $14,000. Because you’re gifting each person $14,000 or less, you don’t have to file a gift tax return.

But if you gift me $20,000 in one year rather than $14,000, then you must file a gift tax return and report the $6,000 in gifts. The gift is not taxable until your lifetime gift exclusion of $5MM (now $10MM under the new bill) has been completely used up. The $6,000 in this example simply reduces your lifetime exclusion by $6,000.

The $10MM will be indexed for inflation and shelters many more estates from federal estate taxes.

Rehabilitation Tax Credit reduced in scope

The rehabilitation tax credit is now only available for certified historic structures. The 20% credit has been retained, however the 10% credit for pre-1936 buildings has been eliminated.

Section 179 is now more useful for commercial property owners

Section 179 allows you to write off the entire cost of certain property. The aggregate cost amount able to be expensed has increased to $1MM, up from $500k. Additionally owners of non-residential property can now use Section 179 for roofs, HVACs, fire systems, and security systems.

"Non-residential property" is commercial property and certain short-term rental property. So if you own a NNN property or an AirBnB property, you may qualify for immediate expensing of big time improvements.

1031 Exchanges now only allowed for real property

The good news is that real estate investors can still use 1031 exchanges. The bad news is that if you have had a cost segregation study performed on your property, you may be in trouble. When you have a cost segregation study performed on your property, you are attempting to assign value to IRC Sec 1245 property, otherwise known as personal property. So the question is, will owners of rental real estate who have engaged in cost segregation studies be able to 1031 exchange their entire property value or just the value associated with real property (not personal property)?

Though the Tax Cuts and Jobs Act removed personal property from qualifying for a 1031 exchange, Footnote 726 of the Committee Report stated “It is intended that real property eligible for like-kind exchange treatment under present law will continue to be eligible for like-kind exchange treatment under the provision.” As a result, we feel Congress intended that 1031 treatment for rental real estate under the law prior to the Tax Cuts and Jobs Act continue to apply.

Ready to take your tax strategy to the next level? Click the link below to schedule a free 30-minute consultation where we'll determine if we can help you save more money.

★★★★★

Hall CPA PLLC, real estate CPAs and advisors, helped me save $37,818 on taxes by recommending and assisting with a cost segregation study. With strategic multifamily rehab and the $2,500 de minimus safe harbor plus cost segregation, taxes on my real estate have been non-existent for a few years (and that includes offsetting large capital gains from the sale of property).